美联储再降息25基点 鲍威尔意外“放鹰”引担忧 市场怎么走

10月30日,美联储最新决议将基准利率下调25个基点至3.75%-4.00%,符合市场预期。但美联储FOMC声明却表明,本次利率决议遭遇“鹰鸽双飞”的罕见局面。随后鲍威尔在新闻发布会上也意外地进行了偏“鹰派”的表态,降低了对12月美联储能否持续降息的预期,引发市场担忧。美联储利率决议公布后,全球主要市场均反应强烈,美股、美债、黄金、加密货币盘中一度急跌,美元拉升。

美联储10月降息如期而至,但为何内部分歧仍无法缓解,鲍威尔意外“鹰派”表态原因是什么,怎么解读,接下来市场走向又如何呢?

一、10月降息如期而至,12月能否持续降息存疑

今日凌晨,美联储公布10月利率决议,将基准利率下调25个基点至3.75%-4.00%,为连续第二次会议降息,符合市场预期。也是自2024年9月以来第五次降息。但随后公布的FOMC声明以及鲍威尔发布会的一系列表态,却降低了12月美联储能否继续降息的预期,引发了市场担忧。据最新CME“美联储观察”,美联储12月降息25个基点的概率为67.8%,维持利率不变的概率为32.2%。美联储到明年1月累计降息25个基点的概率为56%,维持利率不变的概率为21.5%,累计降息50个基点的概率为22.5%。预测市场Polymarket数据显示,市场针对美联储12月利率决议进行押注。本次决议公布之前,市场押注12月继续降息25个基点的概率为90%,决议公布后该概率已降至69%。而市场押注12月暂停降息的概率已升至30%。

本次利率决议公布后,全球主要资产市场反应强烈。美股、美债、黄金、加密货币盘中一度急跌,比特币和以太坊都一度跌超3%。美债收益率全面大涨,2年期和10年期均涨超10基点,美元一度重回99关口上方。英伟达再创新高,收涨近3%,市值突破5万亿美元。最终在英伟达的支撑下,纳指收涨0.55%,标普500指数平收,道指跌0.16%。

市场早已预期美联储10月的降息决议,也期待能够对全球经济和主要资产市场产生刺激。但随着本次FOMC声明和鲍威尔发布会的政策说明,市场对12月美联储能否继续降息存疑,也引发了投资者的担忧。

二、FOMC声明仍显美联储内部分歧

本次美联储FOMC声明宣布将于12月1日结束资产负债表缩减。12月1日结束缩表后,抵押贷款支持证券的赎回本金将被再投资于短期国债。自12月1日起,将对所有到期的美国国债本金支付进行展期。FOMC声明还宣布将贴现利率从4.25%下调至4%,将隔夜逆回购利率由4%下调至3.75%。声明表示,现有数据显示经济正以温和速度扩张,经济前景的不确定性依然较高。今年以来通胀有所上升,仍处于高位。委员会密切关注双重使命两方面的风险,认为就业方面的下行风险已上升。

美联储FOMC声明显示,本次美联储利率决议遭遇“鹰鸽双飞”的罕见局面。美联储理事斯蒂芬·米兰连续第二次会议主张更激进的降息幅度,认为应一次性降息50个基点而非实际落地的25个基点;与此同时,堪萨斯城联储主席施密德则站在鹰派立场反对任何降息举措,主张维持利率不变;其他理事均投票支持本次美联储利率决议。这种出现双向异议的会议上次出现在2019年9月,反映出美联储内部对经济前景的判断正出现显著分化。

FOMC声明表现了美联储内部明显的分歧,说明在美国政府“停摆”期间以及缺乏大量重要经济数据参考背景下,美联储对经济形势的判断以及未来政策如何制定方面缺乏清晰统一的认识。

三、鲍威尔意外“鹰派”表态引担忧

美联储主席鲍威尔随后在新闻发布会上对此次降息决议以及经济形势进行了说明,并回答了记者提问。鲍威尔表示,现有数据表明美国经济前景未有太大变化,正在温和扩张。停摆前的数据显示,经济可能正朝着更稳固的轨道发展;政府停摆将暂时拖累经济活动。他表示通胀水平仍略显偏高,近期通胀预期已有所上升;美联储需要管控通胀持续更久的风险,有责任确保其不会成为持续性问题。就关税问题的影响,鲍威尔表示,在合理的基准情形下,关税对通胀的影响将是短暂的。

针对劳动力和就业问题,鲍威尔表示,劳动力市场似乎正在逐步降温;现有证据表明,裁员和招聘人数仍然偏低;就业面临的下行风险似乎有所上升。他表示,各州失业救济金申请数据传递出一切照旧的信号;失业救济金申请人数较低,表明劳动力市场仅呈逐步降温态势,并未明显快速下滑;如果数据显示就业市场好转,就会影响决策。

针对美联储将结束缩减资产负债表,鲍威尔表示,货币市场压力要求立即调整资产负债表操作;12月将进入资产负债表的下个阶段,短期内将保持稳定。过去三周货币市场流动性趋紧,继续缩表益处不大;银行储备仅略高于充足水平,资产负债表决定给予市场一些适应时间。他表示,已“明显出现迹象”,表明是时候停止量化紧缩了;再投资策略将使加权平均到期期限更接近未偿证券存量。

针对本次美联储利率决议,鲍威尔作了解释说明。鲍威尔表示,经济各领域均未出现明显恶化,总体而言,经济形势一片大好。他表示,认为美联储今年迄今已采取了正确行动。鲍威尔重申,不存在零风险的政策路径,风险平衡已发生转变。美联储降息是“迈向更中性政策立场的又一步”;风险管理逻辑同样适用于今天的降息,10月降息与9月降息具有相同的风险管理逻辑。他表示,美联储无法仅靠一个工具同时应对就业和通胀风险。鲍威尔同时还表示,12月的利率下调“远非”已成定局,暗示美联储不确定12月是否继续降息。

市场对10月份降息的预期已消耗殆尽,仍期待12月美联储能够持续降息以刺激主要资产的继续上涨,但鲍威尔意外偏“鹰派”的表态为市场信心蒙上了一层阴影。

四、如何解读美联储本次决议

针对此次美联储决议,“美联储传声筒”华尔街日报记者 Nick Timiraos评论美联储主席鲍威尔的讲话,他说:“鲍威尔的新闻发布会表明,FOMC整体上并不认同市场此前对12月降息的高度定价。Nick Timiraos表示,10月的FOMC会议在以下方面有些不同。9月的点阵图显示了委员会内的分歧:大多数人倾向于继续降息作为风险管理的手段,但也有相当一部分人认为没有降息的必要。通常情况下,数据可以帮助调和这一分歧。然而,由于在FOMC会议之间少了用来完善前景的高层次数据,因此成员们更少有理由改变立场。

Inflation Insights分析师Omair Sharif认为,美国政府关门以及相关官方经济数据的缺乏可能会阻碍美联储12月连续第三次降息的计划。如果12月10日召开会议时没有反映10月和11月经济活动的官方数据,官员们是否会放心再次降息。他们可能很难就再次降息达成共识,尤其是考虑到9月份点阵图所显示的FOMC内部分歧。

分析师Joseph Richter表示:“在鲍威尔表示12月降息还非板上钉钉后,收益率曲线的熊市趋平,在我们看来有点过头了。”“尽管美联储可能不会在每次会议上都降息(尽管我们认为他们会降息),但我们认为这番言论是在试图重新获得选择权。市场会认为这是鹰派,但这未必能实现。”

纽约梅隆投资管理公司首席经济学家、前美联储高级顾问Vincent Reinhart认为,鉴于数据真空的状况,“数据必须证明进一步宽松是不合理的,这是一个很高的门槛”,因此他补充说,“他们在12月不降息真的很难。继续下去比停下来更容易。”

普渡大学商学院院长、前圣路易斯联储主席James Bullard则认为,12月降息的前景“比市场目前认为的要微妙一些”。他指出,强劲的消费者支出和经济增长,加上近期的通胀挫折,可能成为放缓降息步伐的理由。“你把太多的赌注押在了非农就业报告的放缓上,”Bullard说。他还质疑,政策制定者是否真正适应了每月新增5万个就业岗位就“完全可以接受”的新常态。

此外,特朗普周四对美联储提出批评,再次将矛头指向美联储主席鲍威尔,指责其在降息问题上行动迟缓。特朗普在韩国的演讲中提到“杰罗姆·‘太迟’·鲍威尔”,并表示不会让美联储因担心三年后的通胀而加息。他预计美国经济将在2026年第一季度实现4%的增长,远高于经济学家的预测。此言论突显了特朗普与美联储之间的紧张关系。

五、市场接下来怎么走?

美联储10月利率决议公布后,包括加密货币在内的主要资产市场接下来该如何走呢?市场做出了如下解读。

1. Glassnode 发表观点称,市场持续在短期持仓成本价(约 11.3 万美元)上方挣扎,这是多空双方势头交锋的关键地带。若未能重新站稳该水平,则可能进一步回落至主动投资者实际价格(约 8.8 万美元)附近。Glassnode表示,市场目前的平静是有条件的,但如果美联储的行动偏离预期,这种平静将变得脆弱。

2. Strategy创始人Michael Saylor在接受采访时发表最新比特币价格预测,年底前达到15万美元,未来4至8年目标100万美元。

3. Matrixport发文称,比特币仍处区间震荡;相较之下,美股在AI热潮带动下多次刷新历史高位。与去年曾出现的节奏存在一定相似:在较长时间的低波动整理后,价格曾于约三周内出现阶段性较快上行。当前窄幅波动对交易者的耐心提出更高要求。短线以观望为主,中期格局未变。若美联储维持偏鸽并继续降息,市场更多体现为等待更明确的外部驱动信号。历史上也常见类似节奏:久盘之后,波动会在较短时段内集中释放。

4. 加密分析师@IamCryptoWolf在社交平台发文表示,ETH正在进行扩大楔形回测,之前的阻力位现在充当坚实的支撑位。11月看起来将呈现稳步盘整,月底可能出现突破,12月则加速上涨。

5. Angeles Investments首席投资官迈克尔·罗森表示,这次降息在市场预期之中,但鲍威尔的言论削弱了市场对12月再次降息的乐观情绪。鲍威尔的表态反映出美联储内部在是否进一步降息问题上的紧张局势,尤其是在通胀依然高企并超过美联储自身目标的情况下。投资者应预期通胀可能在较长时间内维持高位,这将限制进一步货币宽松的幅度。受此言论影响,股市出现回落,因为投资者原本预期更多的降息会带来提振。但这只是暂时反应。最终推动股市的仍是企业盈利,而盈利表现依然强劲,因此我们在投资组合中仍保持满仓。

6. 投资公司Aureus Asset Management表示,市场预计美联储至少会在12月之前降息,但通胀上升的风险依然很大。尽管进行了所有关税谈判,但物价仍然很高。我们一直在更多地关注固定收益,我们发现其波动性实际上可以降低,而不是像过去那样只做多股票。

“美联储再降息25基点 鲍威尔意外“放鹰”引担忧 市场怎么走” 的相关文章

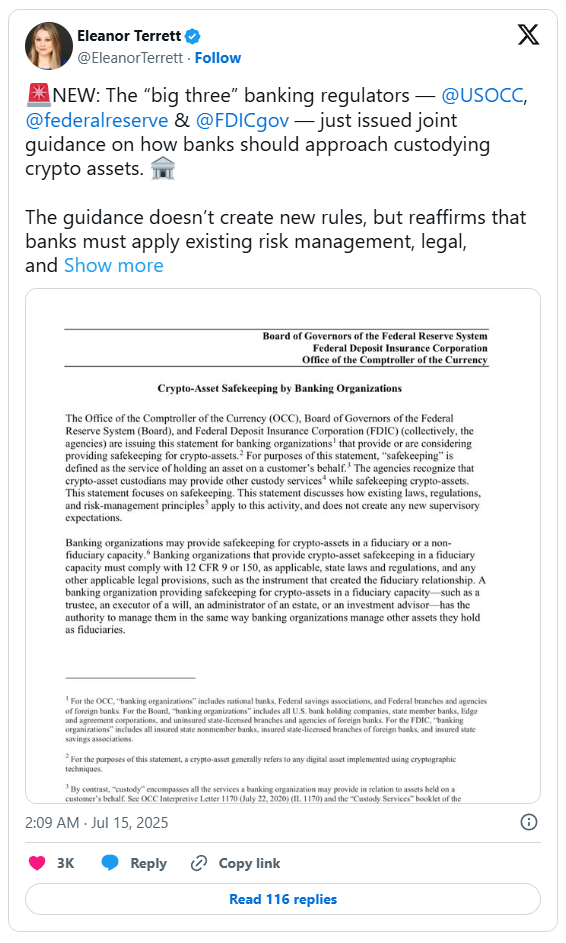

金融迷宫里的新路标;美国银行与数字黄金的看守者游戏

金融迷宫里的新路标:美国银行与数字黄金的看守者游戏标签: 加密货币监管 银行 数字资产托管 风险管理 金融合规目录· 迷雾中的许可:数字资产的看守者· 关键的密钥:责任的重量· 外包的幻象:责任的转移?· 监管者的目光:严苛的审视· 结语:新时代的挑...

WBS注册奖励 | 获取虚拟货币、空投和区块链福利

WBS注册奖励:如何获取虚拟货币、空投和区块链福利?发布日期:2025年7月20日 | 更新日期:2025年7月20日什么是WBS注册奖励?WBS(Web3 Bonus System)注册奖励是区块链项目为吸引新用户推出的激励计划,涵盖虚拟货币(如BTC、ETH)、DeFi(去中心化金融)、NFT(...

比特币主导地位交易观点 | 加密货币市场周期分析与策略

比特币主导地位交易观点:解密加密货币市场周期更新时间:2025年7月27日 | 作者:加密货币市场分析师什么是比特币主导地位?比特币主导地位(Bitcoin Dominance, BTC.D)是指比特币市值占整个加密货币市场总市值的百分比。这一指标是衡量比特币相对于其他加密货币(山寨币)市场影响力的...

超越“数字黄金”;以太坊的无限可能与蜕变之路

超越“数字黄金”:以太坊的无限可能与蜕变之路以太坊 区块链 ETH 智能合约 DeFi NFT Web3 权益证明目录· 以太坊:不仅仅是数字货币,更是全球计算机· 以太坊、以太币与 ETH:概念辨析· 智能合约的魔力:自动化信任的基石· 以太坊的“进化论”:...

东瀛智脑的“数字淘金”:一家日本AI公司与比特币的巨额盟约

东瀛智脑的“数字淘金”:一家日本AI公司与比特币的巨额盟约标签: 比特币 日本企业 加密货币 资产配置 法币贬值目录:· 序章:AI与比特币的奇妙联姻· 量子方案:一项大胆的财务决策· 缘起:法币贬值与全球不确定性· 策略:分阶段投资与香港跳板· 日...

数字资产的“等待游戏”;SEC延迟背后,政治与监管的暗流涌动

数字资产的“等待游戏”:SEC延迟背后,政治与监管的暗流涌动标签: SEC 比特币ETF 加密货币监管 特朗普 真相社交 灰度目录:· 序章:一纸延期,万众瞩目· 延期潮起:SEC的审慎节奏· “加密妈妈”的忠告:耐心是美德?· 特朗普ETF的独特之处:政治与...